The latest news for New Zealand Landlords and Tenants

Credit checks: The vital step that could have saved this landlord $48,000

Are you a landlord or property manager?

Do you credit check all of your tenants before letting them sign the lease?

And are these credit checks comprehensive?

If you are a landlord or property manager your answer to all of the questions above should be yes. Why? Because the cost of not doing a credit check on a tenant is expensive, especially in situations where something goes wrong. Creditchecking tenants has also recently become an insurance requirement for many landlords so not doing one could result in penalties for your home cover.

Doing a credit check is an important step when selecting tenants and it is now something you can do online. Background and credit checking services allow you to easily conduct a comprehensive check for a cost. Although you may not want to pay for this service at the start, it is important to realise how much it could actually be saving you in the long run.

To understand what you could truly be saving with tenant checks and why they are important we are going to look at a few things, including:

- Insurance obligations and what their new terms on tenant checks mean for landlords and property managers who do not do them.

- A recent case where not obtaining a credit check ended in a major financial loss for an owner.

- As well as describing the difference between a comprehensive credit check versus a limited credit check and how this can affect the information you are provided with.

Understanding all of these things will help to see why credit checks on all tenants are vital before handing over the keys to your rental. It will also ensure you take the correct precautions to better avoid future issues with your tenant, such as:

- Rent arrears and unpaid rent at the end of a tenancy

- Damage to your property

As well as the effect it could have on your insurance.

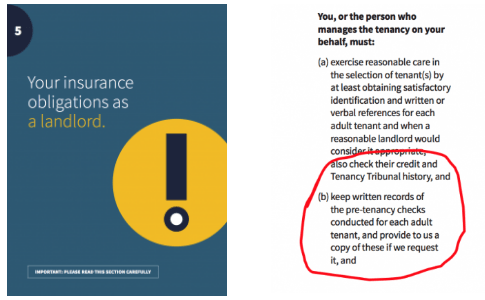

Insurance obligations

What are my insurance obligations as a landlord in terms of credit checks?

February 2019 saw New Zealand’s leading insurance provider IAG update their home policy cover. These changes included making tenant checks a compulsory requirement for every prospective adult tenant.

Recognising credit checks as a small action that could greatly help in reducing tenant selection risks, many other insurance companies followed suit. This includes Vero and Initio who both mentions carrying out and keeping a record of credit checks as “landlord obligations.”

- Vero’s Residential Home Policy (Landlord obligations, p. 19)

- Initio’s Home Policy (Landlord obligations, p. 20)

What happens if I don’t meet these obligations?

It is important to meet your insurance obligations as a landlord with the consequences of not doing so being “invalid claims.”

In order to have a claim that your insurance company sees as valid and as something they will cover you for, you need to meet all of your responsibilities. This is because:

- You agreed to this when signing your policy.

- You prove to your insurance that you have completed all personal risk assessments before letting these tenants live in your home. Therefore, you should be entitled to any and all of the security insurance can provide.

Not completing your landlord obligations can leave you in the lurch when things go wrong. Whether your tenant contaminates your home with methamphetamine or refuses to pay rent, all of these scenarios leave the landlord with big bills to pay on their own if insurance refuses to get involved.

Recent case

New Zealand landlord’s failure to credit check a tenant ends badly

Methamphetamine contamination, one-thousand dollars in rent arrears, and over 48,000 dollars of damage was the result of a nightmare tenant and property manager Yvonne Parker not completing a comprehensive credit check on them during due diligence.

While Parker thought she took correct steps in making sure her prospective tenant would be perfect, this is questionable. This is because the tenant has previous cases with the tribunal which show she owed $5000 to one Whangarei landlord.

All of this is information that a credit check would have revealed as it would search Howe’s name against:

- the Tenancy Tribunal database

- the Ministry of Justice fines database

- and all of New Zealand’s credit agency databases (if it were comprehensive).

Although in an NZ Herald article Parker says she now takes to looking at tenant Facebook profiles during the selection process, this would still not avoid such a situation. Why? Because Facebook does not store credit and fines information and tenants are able to choose what they present on Facebook. This is not the same as with credit reports.

See a photo of the damage done to Parker’s kitchen by the tenant:

Comprehensive vs. limited credit checks

What is the difference between a comprehensive credit check vs. a limited credit check?

A comprehensive credit check searches your tenant’s name against every credit agency in New Zealand, unlike limited credit checks which only search one or two.

A comprehensive credit check also completes a thorough background check on tenants. This is different from looking at their credit and instead, it pulls information about the tenant from:

- the Ministry of Justice fines database

- Tenancy Tribunal database

- social media

- the national media

- as well as other tenant scoring systems like TINZ or illion Tenancy which include the list of criminals being searched for by Interpol, and other relevant information.

The reason we refer to a credit check that does not search all of these things as limited is that the information they provide is lacking – especially when it comes to the information on credit.

What risks do you take when only conducting a limited credit check?

Because some companies only report to one credit agency, you are taking a risk when you only conduct a limited credit check. Why? Because the information that one credit agency has on a tenant is not necessarily the same as other credit databases. This leaves you with gaps in your credit report if you use a limited-service that doesn’t check all three.

An example of this is a recount which showed different results from all credit companies.

- The first from Centrix showed no credit defaults and gave the tenant a great score.

- The second Equifax report showed 2 credit defaults including a repossessed vehicle worth over 6000 dollars and an unpaid life insurance policy.

- The third illion report showed 3 credit defaults. These were the same as the Equifax report as well as an unpaid Genesis Energy bill of over $300.

Although these results don’t necessarily mean this tenant is a bad candidate, it is information that a prospective landlord would want to know. This example also shows that although not every credit checking service searches against all credit databases, you should choose one that does. The reason being is that you risk missing information that could be vital to your final decision.